Too few business owners give succession planning the kind of consideration they do other aspects of their businesses.

Joe ran an injection molding company, the largest employer in the rural town where he lived. When he met business transition expert Lisë Stewart, he was 79, and acknowledged that he needed to get to work putting a succession plan in motion.

He said the same thing a year later, and the year after that, and so on. Finally, four years after she first met him, Joe came to Stewart again. He wanted to put a plan in place immediately. His wife was terminally ill, and he wanted to spend her last few months with her.

“It was too late,” Stewart, the director of EisnerAmper’s Center for Family Business Excellence, says. Instead of passing the business along or gussying it up to sell to a buyer who would keep it going, Joe had to sell off the assets of the business. “Somebody came in and bought the equipment and all of those people in that small, rural town lost their jobs.”

Joe’s story provides one example of why it makes sense for business owners to strategize about the kind of future their company will have after they’re gone, and then work through that strategy to make it a reality. Other unfortunate scenarios, Stewart says, include owners riding to the rescue of their companies after their successors fail, disagreements within families over running the business, and sons and daughters feeling trapped at a company they’re not qualified, or don’t want, to run.

“If I had one thing that I could do in the course of my career, it would be this: I would really like for conversations about succession and transition planning to be just as common in business vernacular as talking about profits, sales, and marketing,” Stewart says.

But too few business owners give succession planning the kind of consideration they do other aspects of their businesses. According to the MassMutual 2018 Business Owner Perspective Study, most business owners say they have chosen a successor, but only about half have a written succession plan, and 1 in 4 say their successor doesn’t know they’ve been chosen.

Tracy Shaw, assistant vice president, business market development at MassMutual, says solid succession planning should be part of business owners’ plans from very early on. “We found that business owners are spending the majority of their time working in their businesses instead of on their businesses,” she said. “It’s never easy to think about how an unforeseen event can impact a business, but in order to raise awareness about these longer-term issues, business owners need to be confronted directly with the potential risks.”

“You know the old adage, you start with the end in mind.”

According to a MassMutual research, the ideal time to work on putting a succession plan in motion is 20 years before there will be a change at the top.

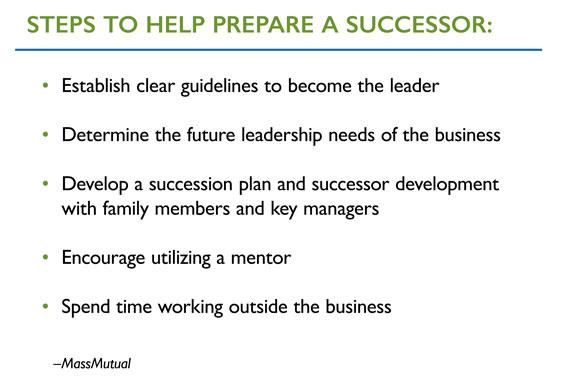

The six points a succession plan should address:

- Goals. Identify what you want to get out of the business and what you want the business to be when you’re gone.

- Your successor(s). Choose who could take over for you when you’re gone and put a management plan in place to make sure they’re ready.

- Management. Define the steps needed to put strong non-owner management in place to help ensure smooth transition.

- Ownership. If there are to be multiple owners in the future, define ownership percentages and roles.

- Transfer. Define when and how the transition will take place and what needs to happen leading up to that transition.

- Finances. Define where the funds will come from to buy you out, calculate tax implications, and the impact of the change on your estate plans.

“The one stat we didn’t need research to prove was that 100% of owners exit their businesses—either by design or by default,” Shaw says. “The choice business owners need to make is either to acknowledge that fact and approach it thoughtfully, or let events overtake them.”

Stewart acknowledges that thinking in such terms is tough to do. Many business owners, she says, don’t really plan to retire, and some shy away from proper planning for fear of being pushed out.

But planning well in advance and carrying through on the strategy is good for the business, the business owner, and their family — whether or not someone in the family is the expected successor.

Stewart is working with a large manufacturing company in its second generation of family leadership. “I think this is a company that’s really doing it right,” she says.

The CEO has children working in the business, but he recognizes that in order for his offspring to be good leaders, they need to go through an in-depth leadership program.

The first thing this CEO and Stewart did was come up with a strategic leadership plan. They have used the strategic plan to develop an internal leadership training program to include the children, but also other leaders in the company, since the CEO recognizes that his children may not be the right leaders for the future. He has also formed an advisory board, so he has input from outside the company in order to avoid the insularity that can plague family businesses.

This CEO recognizes the next generation may not have the same hard-charging style that he has but is creating an environment for their success.

“The ability to recognize that … and actually do something with it, is a rarity,” Stewart says. “I think having some personal knowledge of how you as a leader in the company may need to change and become more of a mentor or coach yourself and get out of the way so that other leaders can grow is an important aspect of grooming this next generation. It’s not easy. I would say that in 10 years, he’s going to have a really nice selection of people who will be well-positioned to run the business in some way.”

—

This article was published on Bizjournals.com/.

Retrieved from https://www.bizjournals.com/bizjournals/news/2018/07/09/how-solid-is-your-succession-plan.html

By Kent Bernhard · July 09, 2018