The most successful financial institutions depend on generating non-interest income to solidify overall profitability. Did you know that bank-owned life insurance is one of the simplest and most effective methods that a bank can use to enhance its non-interest income?

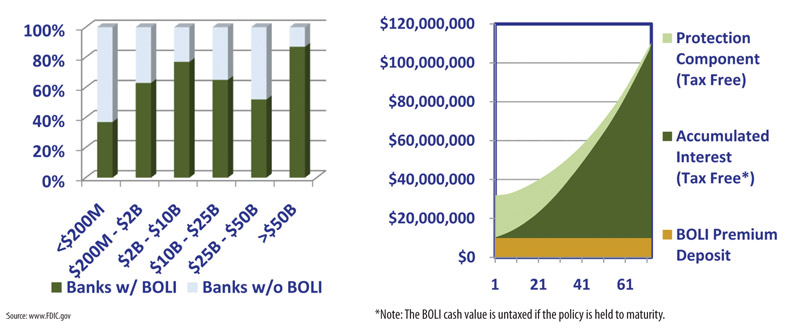

Bank-owned life insurance is not new. Approximately one out of two U.S. banks own BOLI today. BOLI is simply an institutionally designed, key person life insurance policy; it performs like a tax-free investment. Though bank-owned life insurance may possess characteristics similar to that of a bond or a loan, the uniqueness of BOLI is that it is in fact life insurance, possessing a valuable protection component.

The bank typically purchases BOLI with a single premium deposit, insuring a select group of officers or directors. The bank is the owner and beneficiary of the BOLI asset. BOLI contains a savings element (cash value) and a protection component. The cash value includes the BOLI premium deposit plus accumulated interest.

Banks purchase BOLI for some or all of the following business purposes:

- Reason #1: As a tax-favored asset to increase earnings and off set rapidly rising costs of employee benefits (e.g. sky rocketing medical insurance premiums).

- Reason #2: As a means to protect (indemnify) the bank from the unexpected loss of skilled and valuable executives. This is often referred to as key man life insurance.

- Reason #3: As a vehicle used to finance the cost of providing a deferred compensation plan for key officers.

- Reason #3.5: Lastly, as a byproduct, BOLI enhances non-interest income.

Under GAAP, accounting for BOLI is based on the guidelines of FASB Technical Bulletin 85-4. Cash value is recorded as an “other asset.” The monthly policy income is booked as non-interest income. BOLI earnings are reported on the income statement and thus contribute directly to shareholder value.

Generally, there is no initial change in a bank’s balance sheet due to a BOLI purchase (no negative impact on retained earnings). The bank is merely trading one asset for another.

BOLI is carried on the balance sheet as an earning, long-term asset. If the BOLI purchase is for the purpose of financing a deferred compensation plan for key officers, the bank must also account for the benefit liability in addition to the BOLI asset.

BOLI may not make sense for some banks. If a bank is not profitable or has liquidity issues, a BOLI purchase may be inappropriate. Also, if a bank is not comfortable purchasing a long-term asset, then a BOLI program may not be suitable for that institution.

“Life Insurance holdings can serve a number of appropriate business purposes. because the cash flows from a BOLI policy are generally income-tax free if the institution holds the policy for its full term, BOLI can provide attractive tax equivalent yields to help offset the rapidly rising cost of providing employee benefits.”

— OCC 2004–56, Interagency Statement on the Purchase and Risk Management of Life Insurance

BOLI programs are primarily governed by guidelines issued in the Interagency Bulletin on Life Insurance OCC 2004-56. The guidelines assert that risk assessment and risk management are vital components of an effective BOLI program. In addition to conducting a thorough pre-purchase analysis, banks must monitor BOLI risks on an ongoing basis.

By working with a BOLI specialist, the details will be handled efficiently with limited time required by the financial staff of the bank. It is important for a bank to consider using an independent third party administration firm to handle the oversight of the ongoing regulatory due diligence and accounting work. Together, working with the BOLI specialist, checks and balances will be in place to satisfy the needs of the financial institution and its regulatory authorities.

It has been proven that BOLI can play a major role in a bank’s success in capturing non-interest income. As the board and bank management periodically assess and evaluate their game plan, the bank may want to consider incorporating BOLI as a part of its strategy.

Bank News – June 2011 – www.banknews.com